|

Follow Me On: |

|

Jeannie O'Grady Mortgage Loan Originator, NMLS #209607 Creative Mortgage Lenders, NMLS #247952 Phone: Cell/Text: (727) 542-7001 Fax: (727) 823-0687 License: 209607 Jeannie@CreativeMortgageLenders.com www.CreativeMortgageLenders.com |

|||

| ||||

November 2009

|

Are You In for a Trick or Treat? Learn What Remains for Those Seeking a Home or Loan

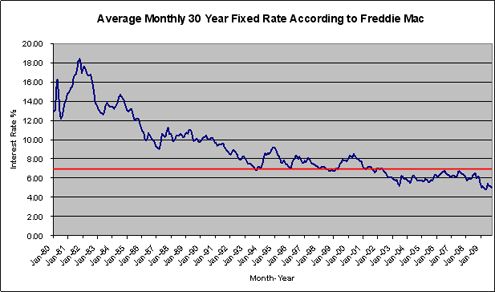

The last weekend in October you were likely treated to a host of Halloween characters, all in search of treats, not tricks. People searching for a new home or a mortgage, whether they donned a costume or not, may have gotten a little of both. Home loan seekers have been treated to great rates all year long since the Federal Reserve announced it would be purchasing mortgage backed securities, with rates diving below 6.00% since last December. However, if you are looking to buy a home, according to the Case-Shiller index, home prices increased for the fourth straight month, possibly signaling the end to home price declines. So, the question now is what lies ahead? How About a Little Perspective? Perhaps this could be for one of two reasons. The first could be that anyone who could refinance into a sub-5.00% rate had already done so. The second is that people could be thinking that either rates will fall below 5.00% again or that rates in the low 5.00% range are simply not that attractive. If we were to take a look at home loan rates dating back to 1980, a span of nearly 30 years, the average monthly reported rate for a 30 Year Fixed Rate loan according to Freddie Mac was 9.07%. While the thought of a rate in the 9.0% range seems exorbitant today, today's rates were inconceivable prior to 2001…and especially in October 1981 when rates were a whopping 18.45%! The chart below shows the average reported monthly interest rates since January 1980. This graph does not take into account the amounts paid to obtain these rates, which were as high as 2.6% in 1984, compared to 0.7% in 2009. The red line represents 7.00%, showing that rates below 7.00% were an abnormality prior to 2002.

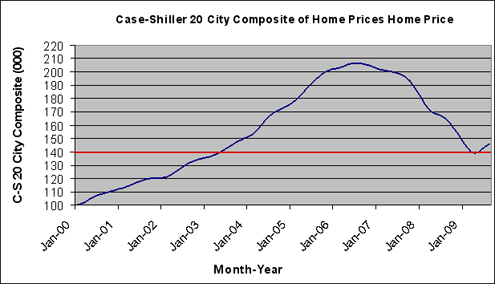

The low rates we have seen this decade are largely attributable to the impact of the 9/11 bombing which launched global economies into a tailspin. The result was an aggressive lowering of rates from the Federal Reserve to stabilize the economy. The impact of low interest rates resulted in a rapidly and unsustainable appreciation in property values. As property values started their return to "normal" we witnessed the plunge into our current recession. We also saw the Federal Reserve get into the mortgage backed securities (MBS) market, becoming the major buyer of MBS this year, driving rates to current and lower levels. While rates may appear a little less attractive based on where they have been this year, do not let that cloud your judgment. Any home loan rate with a five as the first number followed by a decimal point is a fantastic rate, when all things are considered. Just as Halloween Has Passed, So Will These Rates Try These Numbers on for Size Yes, admit it. We have become spoiled with the best home loan rates we have ever seen. Sure, everyone would love a 30 year fixed rate that starts with the number four. However, do not let rates off their lows deter you from making a decision that could save you thousands of dollars over the time you may have your next loan in effect. What about Home Prices? Indexed to 100 in January 2000, it is easy to see when home prices began their rise and how they became out of sorts with where they should have been. It's also easy to determine when home prices started their decline in mid-2006. The chart below, showing a 20 city composite of home prices, also demonstrates what many like to point to in order to demonstrate that home prices have bottomed and are on their way to stabilization and appreciation. The last four months have each marked an increase in month over previous month comparisons; although still lower than the 12 month previous number that is often used for comparison. The red line indicates the point that many are referencing as the bottom of home prices. Whether you are a buyer looking to take advantage of prices not seen since 2003 or a homeowner looking to refinance, this point of reference could be the trigger you need to make a decision to move forward. No one wants to pay more for a home than they could have and increasing values hopefully will make it possible for more people to rid themselves of higher priced loans.

Whether housing has made a bottom or not, first time home buyers (FTHB) have voted with their wallet, showing that home prices overall are now affordable and they have been buying en masse. Washington and the IRS, FTHBs have accounted for monthly sales volume as high as 50% or more of total sales this year. What Now? However, in order to make the best decision and take advantage of rates that historically will be viewed as the lowest we may see in our lifetime, sooner is better than later to pick up the phone. Regardless of what happens to home prices, we do know that interest rates are on the rise. The Federal Reserve will end their program for purchasing MBS next March putting pressure on home loan rates to rise. Go on, pick up the phone, call your mortgage professional and say "Trick or Treat!" Sure, you might be a little late according to the holiday calendar but you just might find something to be thankful for. | ||||||||||||||||||||||||||||||

Content provided by Jeannie O'Grady, your reliable and friendly Mortgage Loan Originator. Programs and information are subject to change at any time and without notification. Please consult Broker for details You are receiving a complimentary subscription to YOU Magazine as a result of your ongoing business relationship with Jeannie O'Grady. While beneficial to a wide audience, this information is also commercial in nature and it may contain advertising materials. INVITE A FRIEND to receive YOU Magazine. Please feel free to invite your friends and colleagues to subscribe. SUBSCRIBE to YOU Magazine. If you received this message from a friend, you can subscribe online. UNSUBSCRIBE: If you would like to stop receiving emails from Jeannie O'Grady, you can easily unsubscribe. Creative Mortgage Lenders, NMLS #247952 |

P.O. Box 76482 St. Petersburg, Florida 33734 Powered by Platinum Marketing © Copyright 2024. Vantage Production, LLC. | |||||||||